{kind=link}

74% of my home costs go to non-home based expenses.

Also, please note that property taxes in my home state of Texas are some of the highest in the nation. Even then, I’m shelling out a good $300/mo on insurance.

Which means the monthly cost of home ownership in an ostensibly low-cost-of-living state is:

-

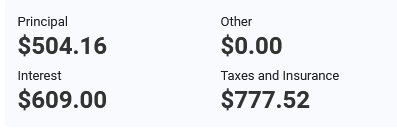

$609 - The Bank

-

$504 - The House amortized over 30 years

-

$470 - The state of Texas / city of Houston

-

$307 - Insurance Company

And please note that this is fucking cheap for my area. $1900/mo was a steal when I nailed it down back in 2018. But the $500/mo that actually goes to the actual house would have been even better. One might even argue it is the real material cost of living. Maybe add in another $400 or so if you squint and don’t ask how much is just going to Cops, Cops, and More Cops or inquire too hard about the state of our streets or schools.

But every time I pay my note, I’m forced to reconcile with this and think about all the people who are told they’ve been “priced out”.

that insurance is wack attack. my shit (locked in early 2021 at a low rate) works out to like

i’m in a position to put extra money each month towards my mortgage, so i do. this is considered “dumb” by much of the PF community compared to putting it into a HYSA or, even more cringe, The Market™. though it should be noted i have looked up my marginal tax rate because any income i generate is subject to income tax, whereas saved interest on early payoff of a loan is not. i also do not give a fuck and would rather pay down the house note. because check this shit out… by making an additional contribution to the principal each month (effectively double), i cut down my loan payoff date by something insane like 14 years off a 30 year note and save a metric assload of interest.

i make roughly the median income in a LCOL area, so all this shit is penny ante. not complaining though. im in my mid 40s and for the first time in my life i don’t have a landlord. and i can do shit to this place. like fix things up better than they were and improve energy efficiency.

i haven’t crunched the numbers on what it would be like with interest rates being like 2.5x higher now, but considering that my stomach was in knots during the closing when they were much lower, i would probably be losing my shit now.

EDIT: i did a 2 year financial breakdown of expenses averaged out to the day (as an average daily expense), and the ratios were:

the overpayment straight to principal means

and keep in mind, this is all back when interest rates were absurdly low compared to other points in US history. i hate all this shit. sometimes i feel like i go through all this deep financial analysis of my situation just to be able to assign a number to how much i hate this shit.

Wife and I spent a year building a house during lockdown. Two months before closing rates suddenly shot up over 5%. They weren’t offering locks right away so we got fucked.

jesus, that sucks