“Credit Score” exists purely to sell you more credit score. It’s only there because they were forced to let you see your own credit history, and they figured “why not monetise that somehow”, so now you’ll be bombarded with ads for more credit and loans, which boosts your “score” while giving them a sliver in affiliate fees.

Actual lenders will examine your credit history, and apply their own score. The criteria for a phone contract, am unsecured bank loan, a mortgage, etc, will all have wildly different requirements. I have one credit card that I pay off each month, and that was enough to get a house.

Paying what you owe reliably is all they’re really looking for.

I just use credit for everything and hover in the 820s. Unless there’s some substantial discount for paying cash I just don’t see the point these days.

That being said, my wonderful credit score ain’t doing shit for me. It’s not like I get some magical super low interest rate. Maybe when things calm down it’ll be worth it, but then there will be some other reason not to borrow money.

There are some nice perks to good credit outside of interest. It can qualify you for better housing, better perks on certain rentals, not having to worry about emergency situations killing your savings outright, and let’s you take advantage of stuff like cash back and bulk purchasing discounts. An example is staple foods, being able to hit the once-a-year bulk deals on stuff like rice or Lawreys garlic salt can cut the price of those items in half or better (personal examples, but the thought should hold). Ancillary perks, but they do add up.

Credit cards come with fraud protection and help you build a credit score, which will get you a lower interest rate on a loan, if you need one. So long as you only spend money you have on hand, and pay off your card every month in full, there’s no down side.

is this a universal thing or are you just assuming that the entire world works like the US? Here in sweden i have never heard of anyone actually using a credit card.

The debt industry makes so much god damned money for the companies involved in it, it’s not even funny.

Between student loans and credit cards, US citizens have a collective $1.73 trillion in debt. And let’s just assume 15% interest on average (probably a low-ball to be honest): that’s $173 billion going to these companies in interest payments per year.

Shit won’t change here because too many people with too much power are making too much money.

In all fairness, it’s not exactly something people talk about - and for the record, I’ve never ended up paying any interest on the card. It’s just convenient, offering a layer of protection for charges, makes it easier for me to track spendings, and allows me to be earning interest on my paycheck by keeping it in a savings account until I need to balance the CC.

{kind=link}

Why even use credit at all? What is wrong with debit?

I use my credit cards for everything I purchase because I get some cash back or other incentives along with fraud protections.

My brother’s a psychopath who plays his credit score like it’s a game so he has like ten cards and a 800+ score he’s proud of.

I make nearly three times as much as him and it took me forever to get an 800 so maybe he’s onto something but fuck that game.

I believe when you get serious about the tactics it’s called churning and manufactured spending

“Credit Score” exists purely to sell you more credit score. It’s only there because they were forced to let you see your own credit history, and they figured “why not monetise that somehow”, so now you’ll be bombarded with ads for more credit and loans, which boosts your “score” while giving them a sliver in affiliate fees.

Actual lenders will examine your credit history, and apply their own score. The criteria for a phone contract, am unsecured bank loan, a mortgage, etc, will all have wildly different requirements. I have one credit card that I pay off each month, and that was enough to get a house.

Paying what you owe reliably is all they’re really looking for.

While you were at parties, I studied the FICO.

Under my tutalage, I have elevated my husband into the ranks of the >800.

I just use credit for everything and hover in the 820s. Unless there’s some substantial discount for paying cash I just don’t see the point these days.

That being said, my wonderful credit score ain’t doing shit for me. It’s not like I get some magical super low interest rate. Maybe when things calm down it’ll be worth it, but then there will be some other reason not to borrow money.

There are some nice perks to good credit outside of interest. It can qualify you for better housing, better perks on certain rentals, not having to worry about emergency situations killing your savings outright, and let’s you take advantage of stuff like cash back and bulk purchasing discounts. An example is staple foods, being able to hit the once-a-year bulk deals on stuff like rice or Lawreys garlic salt can cut the price of those items in half or better (personal examples, but the thought should hold). Ancillary perks, but they do add up.

Credit cards come with fraud protection and help you build a credit score, which will get you a lower interest rate on a loan, if you need one. So long as you only spend money you have on hand, and pay off your card every month in full, there’s no down side.

is this a universal thing or are you just assuming that the entire world works like the US? Here in sweden i have never heard of anyone actually using a credit card.

Yeah great point, the US has a very high emphasis on debt, for horrible reasons.

The debt industry makes so much god damned money for the companies involved in it, it’s not even funny.

Between student loans and credit cards, US citizens have a collective $1.73 trillion in debt. And let’s just assume 15% interest on average (probably a low-ball to be honest): that’s $173 billion going to these companies in interest payments per year.

Shit won’t change here because too many people with too much power are making too much money.

Hi!

I’m the Swede with a CC, right here :)

Now you’ve heard of someone using one (mwahahaha)

In all fairness, it’s not exactly something people talk about - and for the record, I’ve never ended up paying any interest on the card. It’s just convenient, offering a layer of protection for charges, makes it easier for me to track spendings, and allows me to be earning interest on my paycheck by keeping it in a savings account until I need to balance the CC.

Why even use debit at all? What is wrong with bank notes?

Why even use bank notes at all? What is wrong with precious metals?

deleted by creator

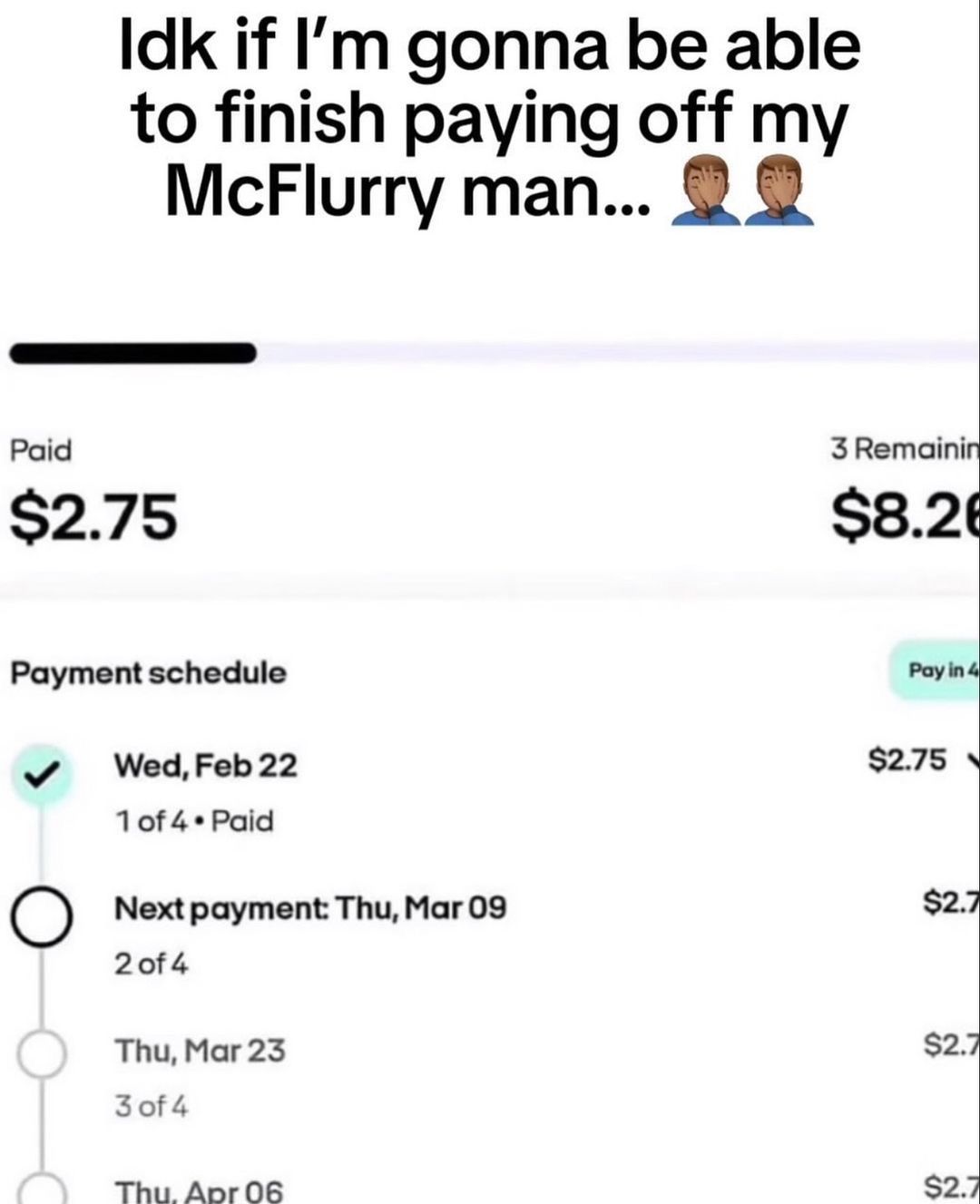

It’s for people who don’t have enough in their bank account.

Although if you don’t have $8, maybe rethink that shitty fast food.

It’s also good for safety.

Getting your credit card stolen and emptied? That’s your creditors problem (generally speaking).

Getting your debit card stolen and emptied? That’s your problem.