If you have a 401(k) or 403(b) through your employer, your employer should be partnered with an investment firm to manage it (e.g. T Rowe Price, Prudential, or Transamerica). You need to figure out which company you’ve got and log in to your account. Ask your HR dept if you can’t figure it out.

That firm will automatically choose where to invest your money unless you log in to your account on their website and tell them where you want it invested.

Most investment firms will offer a limited selection of mutual funds with a variety of objectives. They usually link to each prospectus right there on the site, and the prospectus often has a pie chart telling you where a fund’s investments are located (US, Europe, Asia, etc). It will also list their performance over time, expense ratios, and other useful info, like whether they invest in large vs small cap businesses and their largest individual holdings.

You want to change both where your current investments are allocated and where your future contributions will be allocated.

You also want to try to find funds with low expense ratios (I try to stay below 0.10% unless it’s a fund I really like and am willing to make an exception for). Anything titled “index fund” is likely to be low. Your money is almost guaranteed to be automatically invested in funds with high expense ratios, cutting into your long-term growth, because the investment firm makes big bucks giving your money to people who aren’t wise with it.

If you want to get serious, you can even set up a personal choice account where you can totally independently decide where to invest your money, even in individual stocks. This comes with significant risk and is not a great idea for laypeople like you or I.

Trying to predict the long-term direction of the economy based on short-term market movements is exactly how people lose money in the stock market.

If you’re looking decades ahead, reacting to every short-term fluctuation makes no sense. It’s precisely these knee-jerk reactions that destroy returns. Diversification matters, of course - putting everything into US stocks isn’t wise - but avoiding US stocks altogether because of temporary downturns would be equally misguided if not even more so.

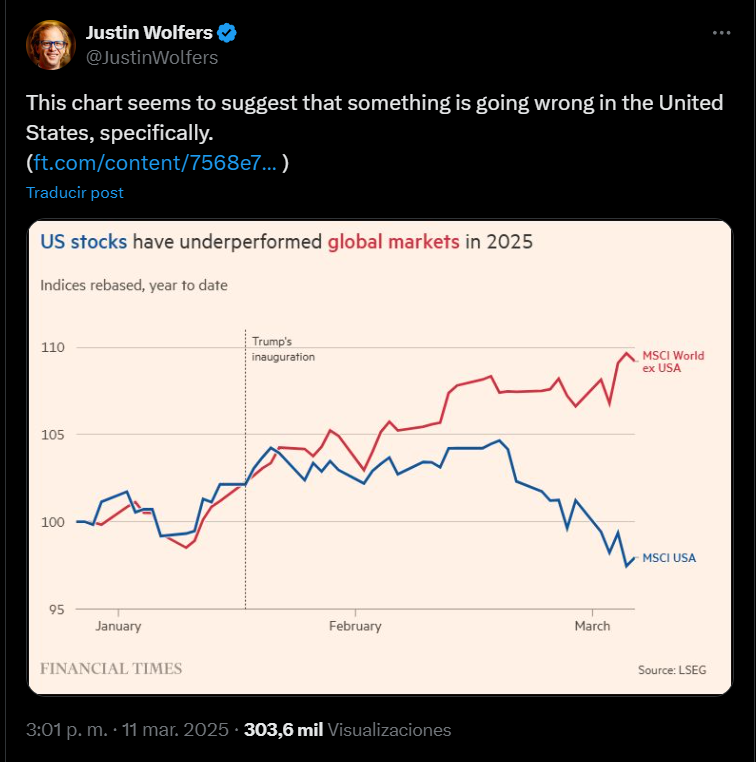

There’s a pretty big leap between “reacting to every short term fluctuation” and moving some of my 403(b) investments to holdings in other countries this one time. While of course we can’t predict exactly how the markets are going to head on a given day, i’s really hard for me to reconcile how you can take a look at what’s happening in the Whitehouse today and think anything but more economic pain for the US is on the horizon. Trump is continuing with the same tariff threats that have already spooked the economy, there are large boycotts of US goods underway among our former allies, government spending is being chopped left and right, putting federal workers and many people who work in grant-funded industries into the unemployment column, and there hasn’t even been enough time for anything I mentioned to hit GDP or unemployment numbers.

I’m very confident about moving toward a diversity of investments while minimizing my exposure to the US economy specifically for the short term. I pay no price to make these trades.

Separately, even if I lose a little money, I’d be fine with that, because this is a good damn political statement too.

think anything but more economic pain for the US is on the horizon.

Probably so - but when I speak of investing, my horizon isn’t five years from now; it’s two to three decades from now. On that timescale, the effects of a Trump presidency will appear as nothing more than a tiny dip on the graph. The roughly 7% average annual growth of the (mostly US) stock market already includes events like the Great Depression, the Dot-Com bubble, the 2008 financial crisis, two world wars, and a global pandemic. If the US economy survived all that, I’m confident it will survive Trump too.

Putting your investments in one place and ignoring them for thirty years is certainly one investment method, but it’s a really good idea to rebalance every year or two to align with global trends and your investment goals.

Well, there I disagree. Aligning your portfolio with current global trends is precisely how many people flushed their savings down the drain when the dot-com bubble burst. Diversification is how you protect your investments against that sort of thing - and true diversification means spreading your investments across time, sectors, and geography. At least, that’s what you do if your goal is to make money, rather than a statement.

I’m diversified across many industries across the entire world with reduced exposure to the US. Comparing this to people losing their life savings in the dot com bubble leads me to think you don’t understand what I’m talking about.

I’m talking about reducing your exposure in a region of the world that looks certain to suffer a lag in economic growth for an extended period. Reducing your exposure in Europe during the start of the Euro Crisis in 2010 was a good idea, and I think reducing your exposure to the US for the near term is also a good idea. Keeping your investments steadfastly in one place without regard for the reality of the world around you is foolhardy. Moving your investments between mutual funds within your 401(k) or 403(b) costs you nothing

{kind=link}

Here in the US, I transfered most of my 403(b) investments into European, Asian, and “emerging market” funds, so I’m happy to be doing my part.

any guidance or resources for an idiot who would like to explore that?

If you have a 401(k) or 403(b) through your employer, your employer should be partnered with an investment firm to manage it (e.g. T Rowe Price, Prudential, or Transamerica). You need to figure out which company you’ve got and log in to your account. Ask your HR dept if you can’t figure it out.

That firm will automatically choose where to invest your money unless you log in to your account on their website and tell them where you want it invested.

Most investment firms will offer a limited selection of mutual funds with a variety of objectives. They usually link to each prospectus right there on the site, and the prospectus often has a pie chart telling you where a fund’s investments are located (US, Europe, Asia, etc). It will also list their performance over time, expense ratios, and other useful info, like whether they invest in large vs small cap businesses and their largest individual holdings.

You want to change both where your current investments are allocated and where your future contributions will be allocated.

You also want to try to find funds with low expense ratios (I try to stay below 0.10% unless it’s a fund I really like and am willing to make an exception for). Anything titled “index fund” is likely to be low. Your money is almost guaranteed to be automatically invested in funds with high expense ratios, cutting into your long-term growth, because the investment firm makes big bucks giving your money to people who aren’t wise with it.

If you want to get serious, you can even set up a personal choice account where you can totally independently decide where to invest your money, even in individual stocks. This comes with significant risk and is not a great idea for laypeople like you or I.

Thank you for the very thoughtful response, I will hopefully get a plan together

Fuck, that’s a good idea.

Thank you.

I did the same with my IRA. I was in VOO but moved to VGK and some short term bonds. So far I’ve saved myself a good amount of money.

Same, babe. Sold all my iShares and Vanguard ETFs and moved into BMO emerging markets, Euro, and Canadian funds.

I still need to look into my employer group pension account. I don’t know how much control I actually have over that.

Trying to predict the long-term direction of the economy based on short-term market movements is exactly how people lose money in the stock market.

If you’re looking decades ahead, reacting to every short-term fluctuation makes no sense. It’s precisely these knee-jerk reactions that destroy returns. Diversification matters, of course - putting everything into US stocks isn’t wise - but avoiding US stocks altogether because of temporary downturns would be equally misguided if not even more so.

There’s a pretty big leap between “reacting to every short term fluctuation” and moving some of my 403(b) investments to holdings in other countries this one time. While of course we can’t predict exactly how the markets are going to head on a given day, i’s really hard for me to reconcile how you can take a look at what’s happening in the Whitehouse today and think anything but more economic pain for the US is on the horizon. Trump is continuing with the same tariff threats that have already spooked the economy, there are large boycotts of US goods underway among our former allies, government spending is being chopped left and right, putting federal workers and many people who work in grant-funded industries into the unemployment column, and there hasn’t even been enough time for anything I mentioned to hit GDP or unemployment numbers.

I’m very confident about moving toward a diversity of investments while minimizing my exposure to the US economy specifically for the short term. I pay no price to make these trades.

Separately, even if I lose a little money, I’d be fine with that, because this is a good damn political statement too.

Probably so - but when I speak of investing, my horizon isn’t five years from now; it’s two to three decades from now. On that timescale, the effects of a Trump presidency will appear as nothing more than a tiny dip on the graph. The roughly 7% average annual growth of the (mostly US) stock market already includes events like the Great Depression, the Dot-Com bubble, the 2008 financial crisis, two world wars, and a global pandemic. If the US economy survived all that, I’m confident it will survive Trump too.

Putting your investments in one place and ignoring them for thirty years is certainly one investment method, but it’s a really good idea to rebalance every year or two to align with global trends and your investment goals.

Well, there I disagree. Aligning your portfolio with current global trends is precisely how many people flushed their savings down the drain when the dot-com bubble burst. Diversification is how you protect your investments against that sort of thing - and true diversification means spreading your investments across time, sectors, and geography. At least, that’s what you do if your goal is to make money, rather than a statement.

I’m diversified across many industries across the entire world with reduced exposure to the US. Comparing this to people losing their life savings in the dot com bubble leads me to think you don’t understand what I’m talking about.

I’m talking about reducing your exposure in a region of the world that looks certain to suffer a lag in economic growth for an extended period. Reducing your exposure in Europe during the start of the Euro Crisis in 2010 was a good idea, and I think reducing your exposure to the US for the near term is also a good idea. Keeping your investments steadfastly in one place without regard for the reality of the world around you is foolhardy. Moving your investments between mutual funds within your 401(k) or 403(b) costs you nothing